Track: Blockchain | Type: Insight | Reading Time: 7–9 min

In technology, the most consequential changes rarely look exciting. They look inevitable.

That is why the London Stock Exchange Group's (LSEG) move toward on-chain settlement matters. It does not validate a culture war about crypto; it signals that tokenization is leaving the experimental perimeter and entering the boring, critical world of market infrastructure. LSEG has publicly outlined plans to build an on-chain settlement capability described as the LSEG Digital Securities Depository (DSD), intended to connect traditional and digital markets and support settlement across multiple networks while remaining interoperable with existing infrastructure.

The story here is not the chain. The story is settlement.

Settlement Is Where Finance Becomes Real

Trading gets the headlines. Settlement carries the risk.

Settlement is the part of the financial system that decides whether a transaction is actually completed, whether cash and securities have exchanged hands, and whether participants are exposed to counterparty failure. In many markets, this process remains slow and expensive because it's built on legacy processes, fragmented ledgers, and layers of intermediaries.

Tokenization proposes a different mechanic: a shared system of record with programmable transfer. If the record is shared and the rules are programmable, settlement risk can shrink — and new forms of market design become possible.

"Tokenization only becomes real when settlement becomes boring."

Why LSEG's Framing Matters

LSEG's public framing emphasizes a specific architectural choice: interoperability. They are linking traditional and digital markets rather than creating a silo.

A parallel system is interesting. An integrated system is investable.

Interoperability changes the calculus for participants:

- Banks can plug into new rails without abandoning existing ones.

- Asset managers can experiment with tokenized instruments without rewriting every back-office system.

- Regulators can supervise a system that still maps to known entities and processes.

The Quiet Pressure Behind the Shift

Institutional movement is usually driven by two forces: efficiency and competition.

Efficiency is the obvious driver. Faster settlement means less capital trapped in transit, fewer reconciliation costs, and lower operational risk.

Competition is less obvious but more powerful. If a credible operator offers a settlement rail that reduces friction, market participants eventually demand access. Nobody wants to be the last firm faxing confirmations while competitors clear instantly.

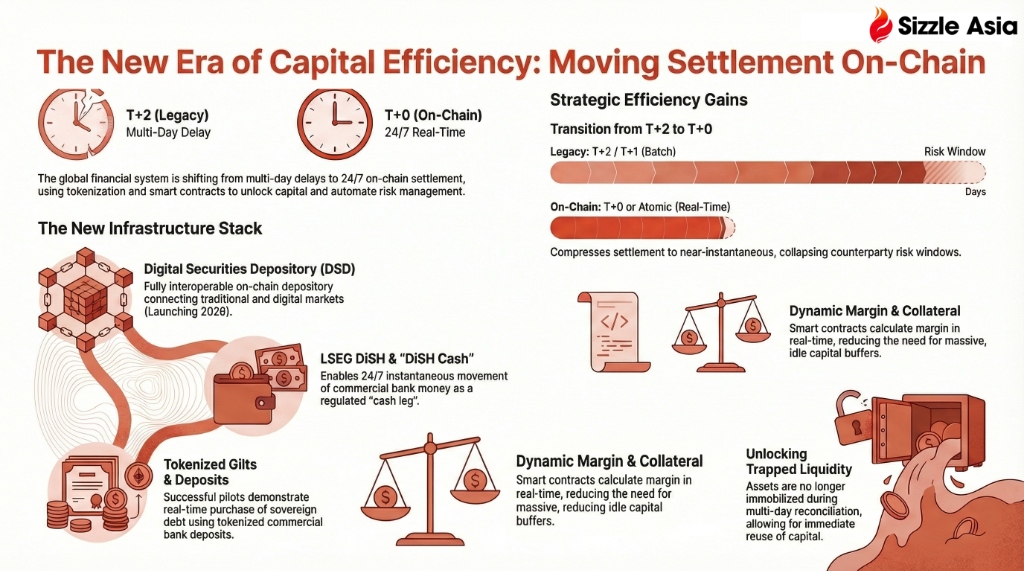

The Institutional On-Chain Settlement Checklist

This is not a "launch a chain" problem. It is a governance and design problem. For institutional on-chain settlement to work, at least four conditions must be true:

-

Regulatory acceptance Who is responsible, and under which rules? The architecture must satisfy legal certainty on ownership and transfer.

-

Identity and permissioning Institutions must know who they are transacting with and under what conditions. That typically implies permissioning, participant controls, and compliance checks designed into the system.

-

Finality and dispute resolution When is settlement irrevocable — and what happens when things go wrong? Institutional rails require clear finality and an operational/legal path for exceptions.

-

Interoperability with cash You cannot settle securities on-chain if the money is stuck in a legacy bank transfer. The cash leg matters. LSEG's Digital Settlement House (DiSH) positions commercial bank money on-ledger to support PvP and DvP-style settlement flows.

Infographic — Institutional on-chain settlement requires regulatory clarity, permissioned identity, finality rules, and a cash leg (DvP/PvP) that can move alongside the asset.

"The future of digital assets is not a new market — it's interoperability with the old one."

What This Means

For investors and editors, the narrative is shifting from "blockchain adoption" to "market infrastructure redesign."

If major depositories and exchanges build on-chain settlement capabilities, tokenization becomes a platform story. Platform stories attract ecosystems: custody, compliance, risk analytics, interoperability layers, and new product design.

The next questions won't be ideological. They will be operational:

Who integrates first? Who sets standards? Who controls the interfaces? And ultimately, who captures the value created by reduced friction?

"If exchanges and depositories move on-chain, everyone else has to choose: integrate or be bypassed."